In the coming debates on tax reform, there will be discussions of the taxes that corporations pay. Compared with other countries, the United States does impose high taxes on corporations.

From CBO:

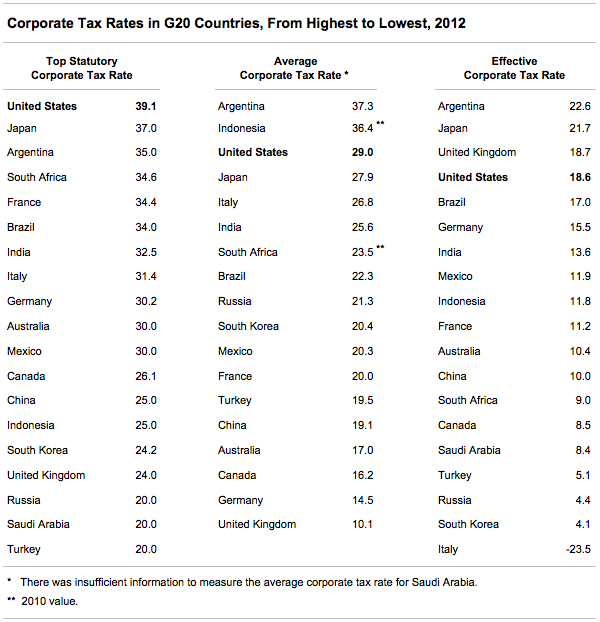

The statutory corporate tax rate is one of many features of the tax system that influence corporate behavior. Companies are likely also to consider other provisions of the tax system—including tax preferences, surtaxes, and noncorporate taxes—that affect the amount of taxes they owe. Among the alternative measures of tax rates that account for some of those provisions are the average and effective marginal corporate tax rates.

The average corporate tax rate is a measure of the total amount of corporate taxes that a company pays as a share of its income. CBO estimates that the U.S. average corporate tax rate for foreign-owned companies incorporated in the United States in 2012 was 29 percent—about 10 percentage points below the top U.S. statutory corporate tax rate.

The effective marginal corporate tax rate (in this document, the effective corporate tax rate), is a measure of a corporation’s tax burden on returns from a marginal investment (one that is expected to earn just enough, after taxes, to attract investors). CBO estimates that the effective corporate tax rate was 19 percent in the United States in 2012. That rate, the fourth highest among the Group of 20 (G20) countries, was about 20 percentage points below the top U.S. statutory corporate tax rate.